Insurance for drug and alcohol rehab is coverage that pays for addiction treatment services, including detox, therapy, and medications. Coverage depends on federal laws like the Affordable Care Act and individual plan details. In New Jersey, Medicaid covers 72% of substance use treatment admissions while private insurance covers 21%, demonstrating the critical role of both public and private coverage in addiction recovery services.

Various insurance plans, including HMOs, PPOs, and public options, determine the extent of coverage for rehabilitation services.

Authorization for addiction treatment by insurance companies relies on established medical necessity and adherence to regulatory standards.

Out-of-pocket expenses for rehabilitation include deductibles, copays, and coinsurance, while alternative payment options encompass sliding scale fees, scholarships, and payment plans.

Will Insurance Pay For Drug and Alcohol Rehab?

Yes, insurance does pay for drug and alcohol rehab, but the scope of coverage depends on your plan and medical eligibility. The Affordable Care Act (ACA) and the Mental Health Parity and Addiction Equity Act (MHPAEA) require most insurance plans to cover addiction treatment at the same level as physical health care, making rehab far more accessible.

Here are some of the key factors of substance abuse treatment covered by insurance:

- Coverage laws: ACA and MHPAEA ensure mental health and substance use services are treated like medical and surgical care.

- The Affordable Care Act and Substance Use Treatment: The ACA requires insurance plans to cover alcohol rehab and substance use treatment. Before the ACA, insurers could deny coverage for addiction based on pre-existing conditions. Coverage varies by plan. Public options like Medicaid can help reduce costs, with eligibility depending on state, income, and family size.

- Mental Health Parity and Addiction Equity Act: The MHPAEA requires group plans with 50+ employees to cover substance abuse treatment and to provide mental health and substance use disorder treatments at parity with medical and surgical benefits.

- Provider network: In-network centers typically cost less, while out-of-network requires PPO benefits.

- Medical necessity: Insurers decide coverage based on assessment of drug use patterns, symptoms, and co-occurring conditions, with weekly progress reviews.

- Public programs: Medicaid and other state-based options lower rehab costs for eligible individuals based on income and location.

What Are The Types of Insurance Plans and Their Coverage for Rehab?

Types of Insurance Plans and Their Coverage for Rehab include Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), and public options such as Medicaid and Medicare. The coverage level is determined by the plan's structure, affecting factors like the need for referrals, choice of providers, and overall out-of-pocket costs.

Here are the common types of insurance plans for drug rehab:

HMOs and Rehab Coverage

An HMO is a health insurance plan that requires members to choose a primary care physician and obtain referrals for specialist care. HMOs maintain a provider network that members must use to receive coverage.

HMOs offer lower-cost fixed premiums but require a referral before specialist visits. Although HMOs can be affordable, referral rules and provider limits reduce convenience for addiction treatment seekers.

PPOs and Rehab Coverage

A PPO is a health insurance plan that allows provider choice. PPO members can access in-network and out-of-network providers, but in-network use lowers costs. PPO plans cost more but provide greater provider choice.

Medicaid and Public Insurance

Medicare and Medicaid cover rehab costs for eligible individuals. Eligibility for Medicare or Medicaid depends on insurance type and personal circumstances. For eligible individuals, public insurance reduces treatment costs and improves access to recovery.

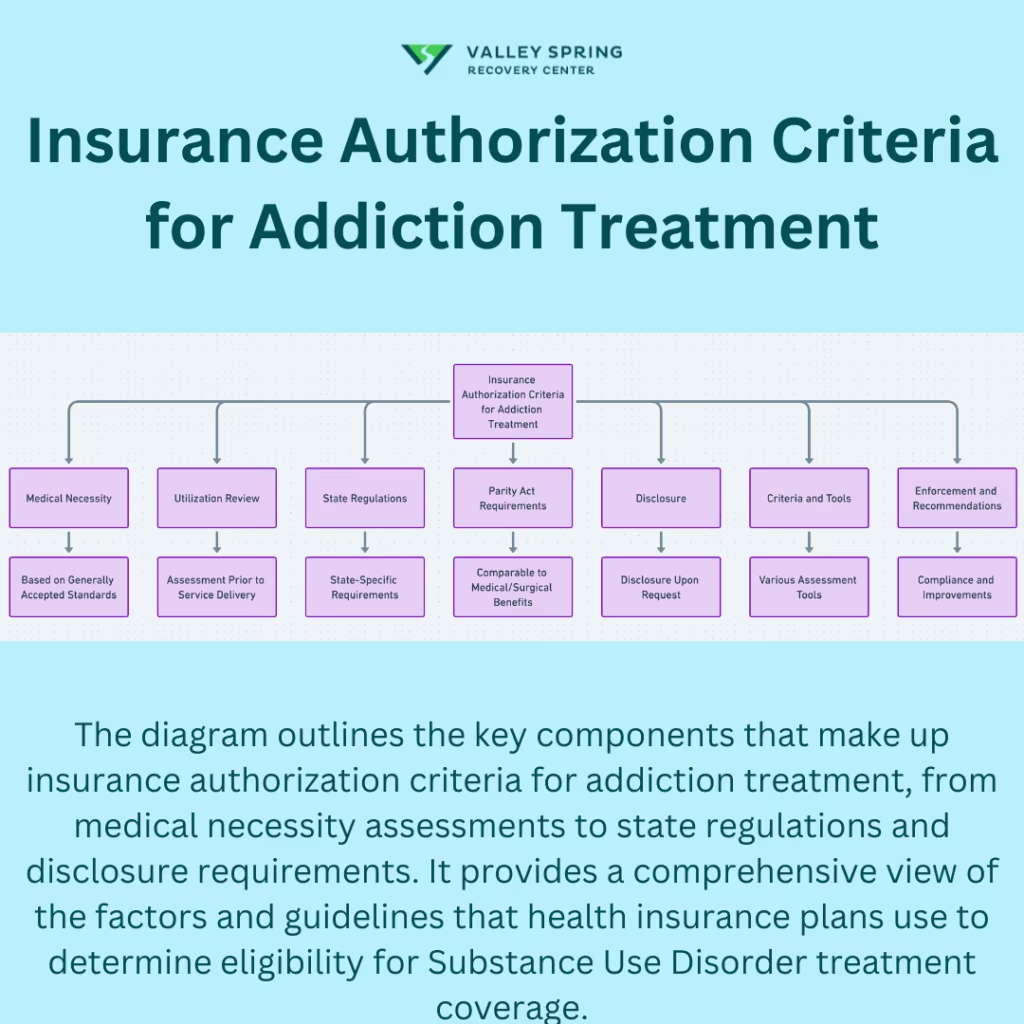

What Are The Insurance Authorization Criteria For Addiction Treatment?

The insurance authorization criteria for addiction treatment are dictated by medical necessity, involve a utilization review process, and must comply with state regulations and the Mental Health Parity and Addiction Equity Act.

Here are the common criteria for addiction treatment:

- Medical Necessity: Health plans determine medical necessity using criteria that align with accepted standards of care. These standards rely on scientific evidence, peer-reviewed literature, or medical community consensus.

- Utilization Review: Health plans use utilization review to evaluate whether recommended treatments meet medical necessity criteria before services begin and throughout patient care.

- State Regulations: As of October 2020, 15 states require commercial health plans to use specific criteria or assessment tools for substance use disorder (SUD) treatment. In addition, 24 states require Medicaid plans to apply medical necessity criteria or assessment tools for SUD treatment.

- Parity Act Requirements: The Mental Health Parity and Addiction Equity Act of 2008 requires health plans to apply medical necessity criteria for mental health and SUD benefits in the same way they apply criteria for medical and surgical benefits. These criteria function as nonquantitative treatment limitations (NQTLs).

- Disclosure: The Parity Act also requires health plans to disclose medical necessity criteria for mental health and SUD benefits to members, prospective members, and contracting providers upon request.

- Criteria and Tools: Health plans often rely on criteria and tools such as the ASAM Criteria, LOCADTR, InterQual Behavioral Health Criteria, and MCG Behavioral Health Care Guidelines to make determinations.

- Enforcement and Recommendations: Enforcement mechanisms ensure compliance with medical necessity requirements, while ongoing recommendations aim to improve the criteria for SUD treatment.

How Can You Find A Rehab Center That Accepts Your Insurance?

To find a rehab center that accepts your insurance, start by checking your provider’s in-network directory or contacting the rehab center directly to confirm coverage. In-network facilities lower out-of-pocket costs, while out-of-network centers may involve higher expenses but sometimes offer payment plans. You can also ask your insurer, healthcare professionals, or support groups for recommendations and use online resources to compare options.

How to Verify Your Insurance Coverage for Rehab?

To verify your insurance coverage for rehab, contact your insurance provider or authorize a treatment center to check benefits on your behalf. Review your policy for details on copayments, deductibles, coverage limits, and any restrictions. Use your insurance card, provider website, or customer service number to confirm what services are covered, for how long, and your financial responsibility. Knowing this ensures clear expectations and informed decisions about treatment.

Will Your Insurance Authorize Coverage Based On The Stage of Addiction?

No, insurance does not authorize coverage solely based on the stage of addiction. Instead, approval depends on medical necessity, which insurers determine through comprehensive intake assessments and DSM-5 criteria. Severity of substance use, daily life impact, past treatment outcomes, and co-occurring disorders all play a role in authorization.

Here are the key factors insurance companies review when authorizing coverage for addiction treatment:

- Policy guidelines define medical necessity standards under each plan.

- Pre-authorization is often required before treatment begins.

- Level of care (inpatient, outpatient, detox) affects approval decisions.

- Duration limits control how long coverage is provided.

- Out-of-network providers increase personal costs.

- Appeals allow patients to challenge and re-evaluate denied coverage.

What Are The Out-of-Pocket Expenses and Alternative Payment Options?

The out-of-pocket expenses and alternative payment options include deductibles and copays, coinsurance, sliding scale fees, and scholarships. Patients can manage costs through various methods, like payment plans and utilizing Health Savings Accounts (HSA) or Flexible Spending Accounts (FSA).

Here are the main out-of-pocket expenses and alternative payment options for rehab, with additional considerations:

- Deductibles and Copays: Most insurance plans require a deductible before coverage starts, and copays for each service or session.

- Coinsurance: After meeting the deductible, patients are responsible for a percentage of treatment costs.

- Sliding Scale Fees: Rehab centers adjust fees based on income, making care more affordable for individuals with limited means.

- Scholarships: Some facilities provide financial aid or grants that reduce or eliminate treatment costs for qualified individuals.

- Payment Plans: Treatment centers allow structured installment payments over time instead of lump-sum charges.

- Personal Loans: Banks or healthcare lenders provide loans for rehab expenses, with terms and interest rates that must be reviewed carefully.

- Health Savings Accounts (HSA) or Flexible Spending Accounts (FSA): Pre-tax accounts help pay for addiction treatment expenses and lower the effective cost.

- Employer Assistance Programs (EAP): Some employers provide partial coverage or referrals through workplace wellness benefits.

- Charitable Organizations and Nonprofits: Grants or vouchers support individuals who qualify for financial assistance.

- State and Community Programs: Public health departments or state-funded rehab programs provide low-cost or free treatment options.

By combining insurance with these payment strategies, individuals reduce financial barriers and receive necessary treatment without excessive economic strain.

What is an EOB Explanation of Benefits?

An Explanation of Benefits (EOB) is a document that health insurance companies send after medical services. The EOB shows services received, provider charges, insurance payments, and patient responsibility. It lists deductibles, copays, and coinsurance amounts. The EOB clarifies what insurance covers and what the patient owes. It is not a bill but a cost breakdown. Reviewing the EOB ensures correct billing and helps patients understand their insurance benefits and out-of-pocket expenses.

Michael O’Sullivan from Valley Spring Recovery Center emphasizes the importance of understanding your EOB in his YouTube video, “Guide To Insurance For Drug Rehab From A Chief Financial Officer.” He explains that the EOB is not a bill but a breakdown of costs associated with healthcare services, designed to provide clarity on insurance coverage and out-of-pocket expenses. O’Sullivan’s insights highlight the need for patients to review their EOBs to grasp their insurance benefits fully and manage their healthcare finances effectively.

Can You Get Life Insurance After Rehab?

Yes, life insurance is available after rehab. Rates depend on medical history, and many insurers require at least three years in recovery. Comparing providers helps secure better policy options.

Can Health Insurance Drop You For Alcoholism?

No, health insurance does not drop coverage for alcoholism. The Affordable Care Act prohibits denial for pre-existing conditions. This ensures individuals receive continued coverage for treatment needs.

Are Drug Rehabilitation Costs Deductible?

Yes, drug rehab costs are deductible as medical expenses under IRS rules. Deductible items include doctor fees, therapy, meals, lodging, and facility treatment costs.

What is the Affordable Care Act, And How Does It Affect Insurance Coverage For Rehab?

The Affordable Care Act is a federal law that expands insurance coverage. It requires plans to include alcohol and substance use disorder treatment, ensuring equal access to addiction care.

Does Insurance Cover Alcohol Rehab?

Yes, insurance covers alcohol rehab. Federal law requires most plans to include substance use disorder treatment, though coverage depends on the policy and provider network.

Do Insurance Companies Pay For Medication-Assisted Treatment?

Yes, insurance companies cover medication-assisted treatment. Coverage includes FDA-approved medications such as methadone, buprenorphine, and naltrexone, combined with counseling when medically necessary.

How To Get Insurance To Pay For Inpatient Rehab?

Getting insurance for inpatient rehab involves documenting medical necessity, completing an intake assessment, and securing pre-authorization from the insurer. For the lowest costs, admission must be to an in-network facility, which ensures coverage according to the plan's benefits.

How Many Times Will Insurance Pay For Rehab?

Insurance will pay for rehab multiple times if medical necessity is established, subject to the limits of the specific insurance plan and the patient's progress reviews. Coverage for subsequent treatments is determined by these factors and is generally maximized when the facility is in-network